Is General US Inflation Accelerating?

The GDP deflator's rate of increase rose in 2025Q4, but was boosted by the government shutdown. Underlying PCE inflation leaves room for more rate cuts.

Sectoral US Inflation

This note examines emerging differences in inflation rates across the various categories of domestic demand, revealed in the latest GDP release. It asks if a recent faster rate of inflation in the GDP deflator is concerning.

It notes the contrasting behavior of goods and services inflation for consumers and calculates the impact of tariffs on US inflation, drawing implications for the Fed. It draws attention to the pickup in the rate of inflation in some investment deflators and in the price of government spending, the latter related to the shutdown.

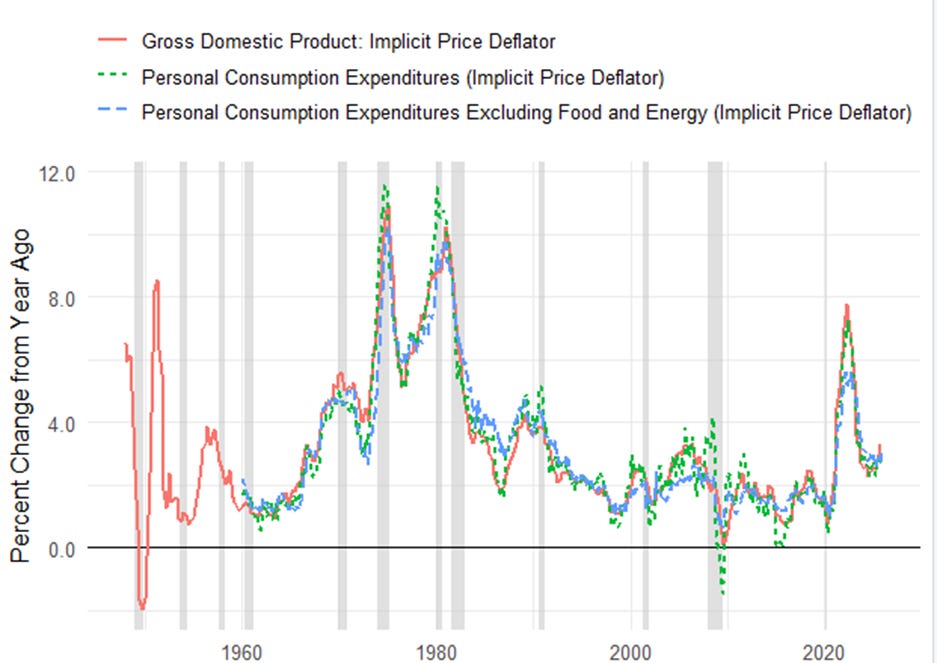

Over the long term, US inflation is a domestic phenomenon. Import prices can have a short-run influence, but since imports are equivalent to only 14% of GDP, domestic price developments dominate, especially as many importers “price to market,” though other domestic producers are influenced by the price of competing imports. Chart 1 shows that PCE inflation, both headline and core, mostly moves in line with the GDP deflator over long periods, but that there can be significant short-run divergences, notably around the GFC and its aftermath.

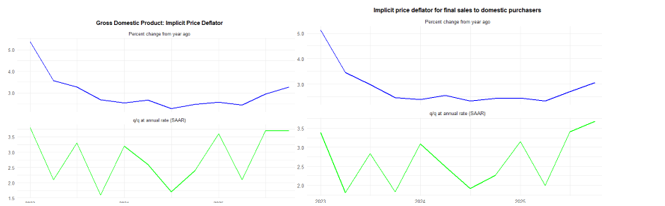

Turning to shorter run developments, we can see that the rate of inflation in the price of GDP picked up in 2025, and this also showed in the deflator of sales to domestic purchasers; both were running close to 3% at end-2025. This was shutdown distorted.

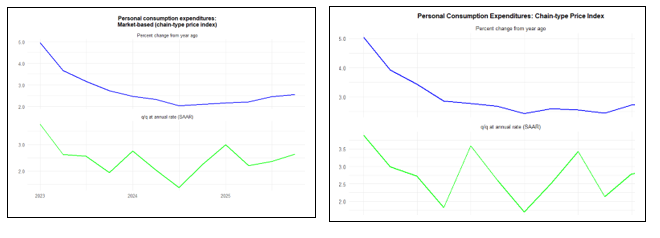

Inflation in the PCE deflator, in total and for market-based prices (i.e., excluding imputed prices).picked up less than for the GDP deflator.

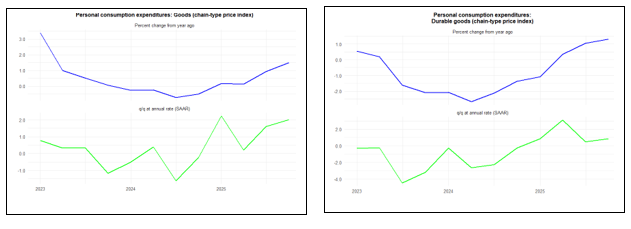

The trends of PCE goods and services inflation diverged. Goods inflation picked up, especially durables, while services decelerated.

If we attribute the rise in the y/y goods inflation rate since 2024, from basically zero to about 1.5%, to tariffs, that will imply about a ½% tariff effect on PCE inflation by end-2025 (goods account for about a third of Personal Consumption Expenditures). Yale Budget Lab also estimated a ~1.5% effect of tariffs on goods prices, while NBER/Harvard pricing lab estimated a 0.7% effect on overall prices in March-August. CBO estimated that tariffs would add 0.4% to inflation in 2025 and 2026. My estimate is broadly consistent with these.

Core PCE inflation was 2.7% y/y in 2025Q4. If we accept an estimated tariff effect of ½% on inflation, then excluding tariffs the Fed is virtually at its 2% target, with services inflation on a well-established downward path. That makes caution about cutting interest rates further look excessive.

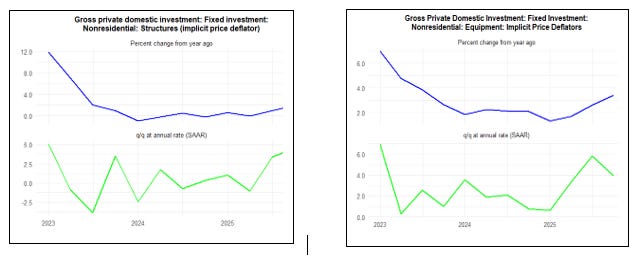

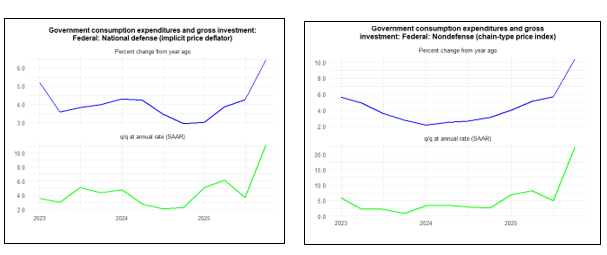

While PCE price inflation looks on a good track in underlying terms, inflation is picking up in non-residential investment and government purchases, though the latter numbers may be distorted by the government shutdown at the end of last year. For investment, the pick up is in equipment rater than structures and software.

The price index for spending on national defense has risen from an annual rate of around 4% in 2024 and early 2025 to 6% y/y and an annualized q/q rate of almost 10% at the end of 2025. The price of non-defense spending accelerated to a y/y rate of over 10% a the end of 2025, with a q/q annualized rate of 20%!

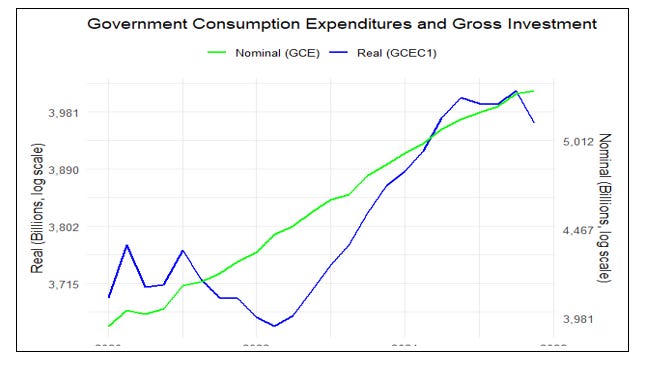

The long-lasting government shutdown distorted these figures. Employees who were not paid for a period still had their wage entitlements recorded on an accruals basis, and later got back-pay. In terms of output, that was measured by the actual hours they worked, so volumes dropped. Accordingly, the price index (nominal spend/real volume of output) was boosted. This faster rate of increase in the government spending deflator contributed to the faster increase in price inflation for GDP and domestic expenditures. The effect should unwind in 2026Q1.

Conclusion

Given that inflation in the US is predominantly a domestic phenomenon, the pick up in the rate of increase in the GDP deflator at the end of 2025 on the face of it could give some reason for concern. However, a good part of this was explicable by the shutdown-related boost to the deflator for government expenditure, which reduced output but not nominal costs. This price boost will be reversed in Q1, so that we should not worry about the Q4 GDP deflator signaling an inflation acceleration.

There are some upward pressures on domestic investment prices, likely explained by strong demand from tech and restricted supply. This not a worry for near term general inflation, though it will impact on profits of equipment buyers and may eventually have some small pass-through due to higher depreciation costs.

The pick-up in the PCE deflator during 2025 is largely explained by tariff effects, which have added about ½% to the rate of inflation. Services disinflation remains solidly in play. Overall, the trajectory of inflation in the core PCE deflator looks consistent with room for more Fed interest rate cuts.